The first task in any real estate investment decision is to build a proforma, which is just a word that means cash flow projection. In this guide, we will define the term proforma, look at an example of a simple real estate proforma, review a more complicated real estate proforma, and also discuss some nuances you may see in the real world. Here’s what you’ll learn:

- What is a Proforma in Real Estate?

- How to Create a Simple Real Estate Proforma

- Simple Real Estate Proforma Example

- How to Create a Detailed Commercial Real Estate Proforma

- Detailed Commercial Real Estate Proforma Example

What is a Proforma in Real Estate?

First, what does proforma mean in real estate? In real estate, the word proforma simply means cash flow projection. The word “pro forma” is Latin for “as a matter of form” and it is a term used to describe the document that lays out a cash flow forecast. The real estate proforma is important because it shows a forecast of all sources of income and expenses for a property, as well as a bottom-line cash flow figure.

Sometimes you will see this term written with two words as “pro forma” and other times you will see it written more concisely as “proforma”. Both are commonly used in the commercial real estate industry and have the same meaning.

Summary

In real estate, a proforma is a document that projects the cash flow of a property, detailing all expected income sources and expenses. The term “proforma” or “pro forma” is derived from Latin, meaning “as a matter of form,” and is crucial for understanding a property’s financial performance and bottom-line cash flow.

How to Create a Simple Real Estate Proforma

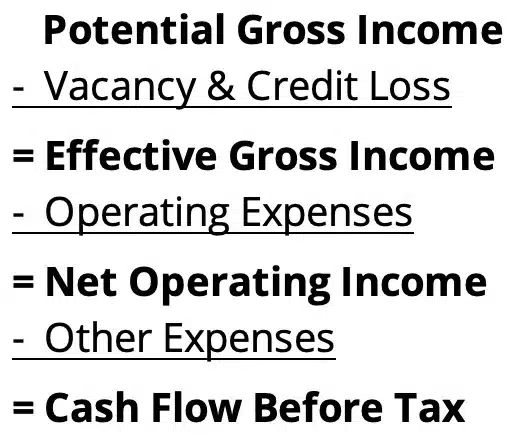

We’ll go through a more detailed example below, but first let’s start with the basic real estate proforma format. This is often what will be created during a back of the envelope analysis, before moving on to a more detailed projection. A proforma can be completed for a single period of time, such as a year, or over multiple time periods. At a high level, a simple proforma is often structured like this:

Let’s look closer at each of these line items.

Potential Gross Income is the primary potential source of income a property could generate if it were 100% occupied. In practice, this consists of income from contractual leases in place, and if a space is vacant then an estimate for market rent is used.

Vacancy is a deduction that accounts for unoccupied space in the building, and Credit Loss is a deduction for non-payment by tenants. These deductions are commonly expressed as a percentage of Potential Gross Income.

The Effective Gross Income is what’s left over after deducting vacancy and credit loss from Potential Gross Income.

Operating Expenses for a commercial property consist of all expenses required to operate the property. Major categories of expenses include property taxes, insurance, maintenance, janitorial, utilities, management, etc.

The Net Operating Income (NOI) is what’s left over after subtracting out operating expenses from the Effective Gross Income. The Net Operating Income, often abbreviated as NOI, is one of the most widely used metrics for a property.

Other Expenses deducted from the net operating income typically include capital expenditures and loan payments. Capital Expenditures are major expenses required to maintain or add value to the property. These could include the replacement of heating and ventilation systems (HVAC), roof replacement, re-paving a parking lot, etc. Debt Service or loan payments are also deducted from NOI.

Finally, the Before Tax Cash Flow is what’s left over after deducting any additional below NOI expenses such as loan payments or capital expenditures.

Summary

A real estate proforma is a financial projection that estimates a property’s income and expenses. It starts with the Potential Gross Income, then deducts Vacancy and Credit Loss to arrive at the Effective Gross Income. Operating Expenses are subtracted from this to calculate the Net Operating Income (NOI), a key metric. Further deductions for Capital Expenditures and Debt Service result in the Before Tax Cash Flow.

Simple Real Estate Proforma Example

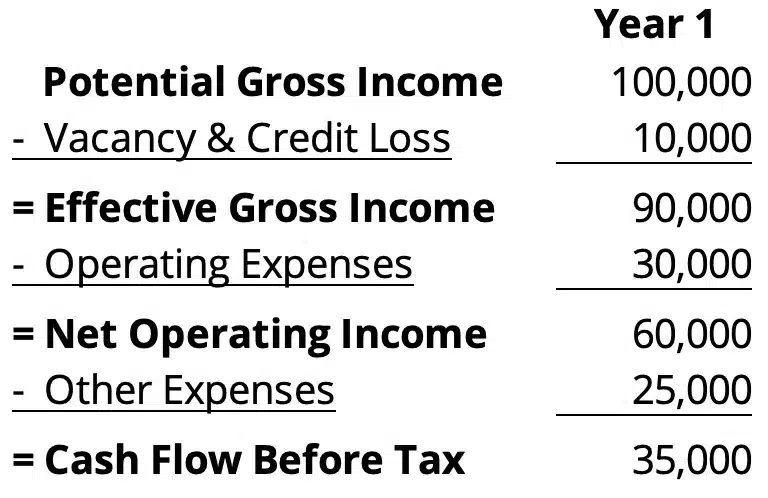

A real estate proforma is often completed for the first year of operations for a stabilized property. Stabilized in this sense just means the property has achieved its long term expected occupancy. This proforma can then be used to quickly calculate some back of the envelope return metrics.

One Year Proforma

Here’s an example of a simple back of the envelope proforma for a single year:

Commercial real estate investors, brokers, lenders, and appraisers often use the net operating income from a simple proforma like this to estimate a property’s market value using the capitalization rate.

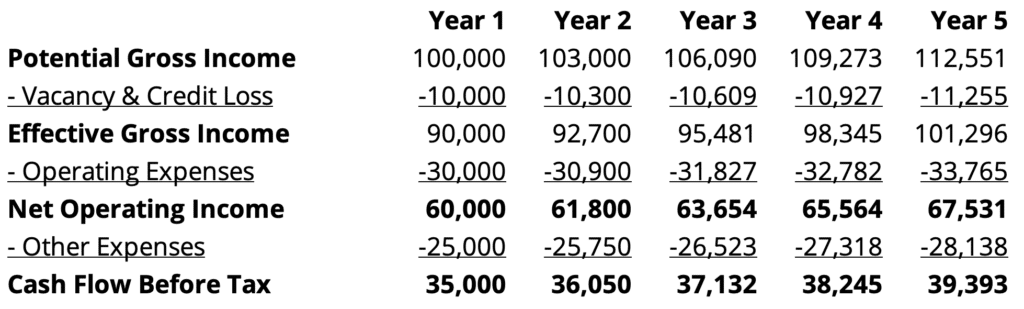

Multi-period Proforma

A simple proforma can also be completed over multiple years:

A multi-period proforma like this is used to estimate cash flows over the entire holding period and gives a more complete perspective on future investment performance. It allows you to analyze different scenarios such as the best case, worst case, and most likely case. You can also calculate financial ratios such as the cash on cash return, equity multiple, operating expense ratio, etc. over the entire holding period.

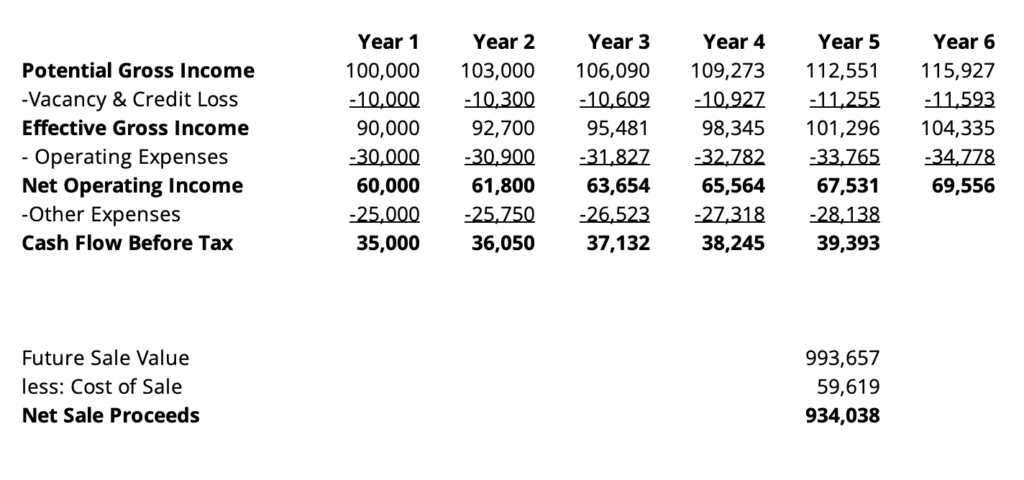

Future Sale Proceeds

An estimate of the future sale proceeds will also need to be calculated in a multi-period proforma. In the commercial real estate industry, future sale proceeds are commonly referred to as the reversion or disposition cash flow, to distinguish from the ongoing operating cash flows of the property.

One way to calculate the disposition price is by applying a cap rate to the net operating income in the final year in the holding period. It is also common to use the NOI for the year after the final year in the holding period, since this will be the first year of NOI for the new buyer. Selling costs such as broker commissions, legal work, etc. can then be estimated and deducted from the future sale price to calculate net sale proceeds.

In the example above, the year 6 NOI is 69,556. We apply our estimated market cap rate of 7% at the time of sale to estimate a future sale price of 993,657. From this, we deduct our estimated selling costs of 6% to arrive at net sale proceeds of 934,038.

Once the future sale proceeds are forecasted along with the operating and investment cash flows, a discounted cash flow analysis can be completed to calculate the Internal Rate of Return (IRR), Net Present Value (NPV), and Modified Internal Rate of Return (MIRR).

Next, let’s add some more context to this discussion and look closer at a more complicated real estate proforma.

Summary

A single-year proforma is used to estimate a stabilized property’s net operating income and market value using the capitalization rate. In contrast, a multi-period proforma forecasts cash flows over the entire holding period, allowing for scenario analysis, the calculation of financial ratios, and a discounted cash flow analysis to determine the Internal Rate of Return (IRR), Net Present Value (NPV), and Modified Internal Rate of Return (MIRR). To estimate the future sale price, a cap rate is applied to the final year’s NOI, and selling costs are deducted to determine net sale proceeds.

Download Real Estate Proforma Now

Fill out the quick form below and we’ll email you your free real estate proforma template.

How To Create a Detailed Commercial Real Estate Proforma

A more complicated commercial real estate proforma will follow the same basic structure discussed above, but will include more detail. Before we dive into an example, it is important to note that the way a proforma is presented in practice will often vary from one project to another. This variation could be driven by differences in the property type, complexity of the project, time frame, sophistication of the parties involved, intended audience, and any other unique circumstances.

For example, a multifamily development proforma will not look exactly like an already built hotel proforma because these are different property types in different stages of completion with different sources of income. The same is true for a condominium project with individual units for sale versus a building occupied by a single tenant with a triple net lease.

For most commercial properties, tenants sign long-term leases that spell out in painstaking detail all the income a landlord will receive. These leases contain all the details needed to reliably forecast tenant income for years into the future. The key is to translate this information “lease by lease” to create a more accurate cash flow projection.

As you can imagine, analyzing a property lease by lease is also more complicated and time-consuming. Leases often contain different terms and conditions, with inconsistent requirements for rent, rent increases, or reimbursements. These differences occur because leases are created at different times, often by different landlords, under different market and tax environments, and are negotiated to reflect the specific needs of each party. To make this process faster and easier, many commercial real estate professionals use specialized lease by lease analysis software.

With that said, let’s take a look at what a more detailed proforma looks like for an office, retail, or industrial property:

A more complicated proforma like this can be completed for a single year or over multiple years, and is often prepared on a monthly basis. You’ll notice these line items are similar to the simple proforma structure discussed above, but include some extra detail.

Summary

A more complex commercial real estate proforma follows the same basic structure but includes more detail, varying based on factors such as property type, project complexity, and intended audience. For most commercial properties, long-term tenant leases provide the information needed to forecast income reliably on a “lease by lease” basis, though this process can be time-consuming due to inconsistencies in lease terms and conditions. Specialized software is often used to streamline this analysis. A detailed proforma, which can be prepared for a single year or multiple years on a monthly basis, includes additional line items compared to a simple proforma.

Detailed Commercial Real Estate Proforma Example

To understand how to read a proforma like this, let’s discuss each of these line items.

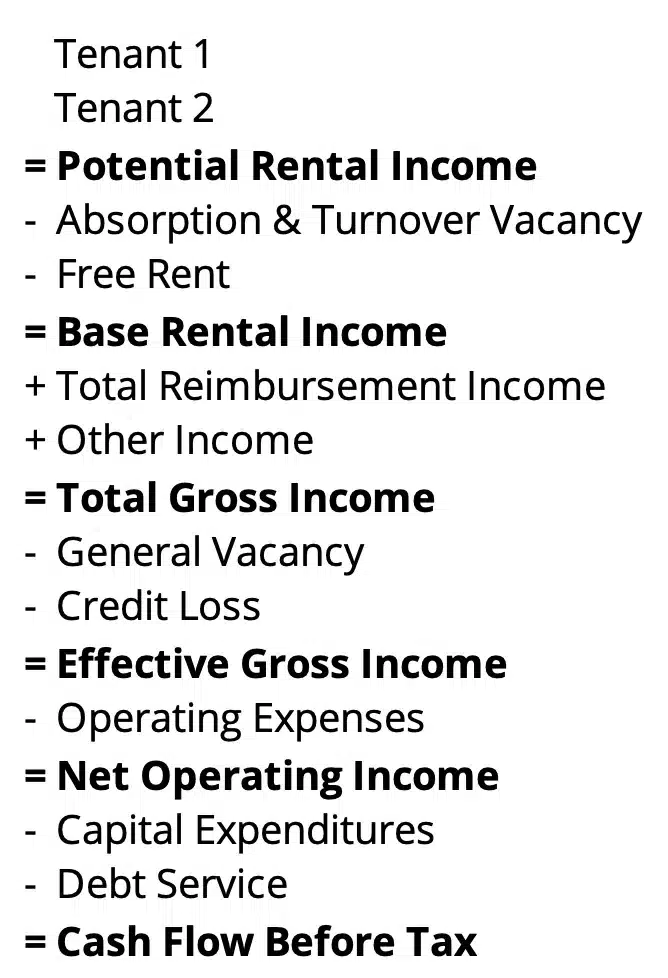

Potential Rental Income

- This is the amount of base rent the property could generate if it were 100% occupied.

- For simple proformas it is calculated by taking the average base rent per square foot in a property and multiplying it by the total rentable square feet. For example, if you have a 10,000 square foot property and the average rent per square foot is $10, then you could calculate a back of the envelope Potential Rental Income of $100,000.

- For more detailed proformas this is calculated “lease by lease”. This entails entering data from each tenant lease from the rent roll using lease by lease analysis software. This will forecast all income under each lease, considering lease start and end dates, rent increases, reimbursement structures, market leasing assumptions after the lease expires, and more.

- Since commercial real estate leases spell out in detail all the income that will be received from tenants in place, creating a proforma lease by lease like this results in a more reliable and accurate forecast.

- Once all the base rent has been calculated for all existing leases in place, then an estimate can be used for any remaining vacant space, including how long it will take for the property to absorb or lease up the unoccupied units. These estimates are informed by a real estate market analysis. This is all added together to show what the potential rental income is for a property, using both in place leases and speculative leases for vacant space.

Absorption and Turnover Vacancy

- Absorption is the actual vacancy of the property due to the time it takes to lease up vacant space.

- Turnover vacancy is the downtime between leases that occurs when an existing tenant does not renew its lease, and therefore the unit sits empty until a new tenant is found.

- For simple proformas a detailed absorption and turnover vacancy calculation is usually not considered. Instead, a general vacancy deduction is often used, which we’ll cover in more detail below.

- For more detailed proformas, once all the leases have been entered, this can be automatically calculated based on the actual vacancies that occur according to the lease start and lease end dates.

- Since the Potential Rental Income line item calculates rent assuming a property is 100% occupied, this absorption and turnover vacancy line item is important because it will completely offset the potential rent shown for the space that is actually unoccupied.

Free Rent

- This is the dollar amount of free rent, also known as abatement or concessions, sometimes given to tenants to motivate them to sign a lease.

- It is another deduction made to the Potential Rental Income to figure out the actual money received by the landlord or owner of the property.

Base Rental Income

- This is calculated by taking the top-line Potential Rental Income and deducting absorption and turnover vacancy and free rent.

- It shows the amount of base rent that is expected to be collected or realized by a landlord or owner.

Reimbursement Income

- Tenant leases in office, industrial, and retail properties usually have some sort of expense reimbursement structure. Reimbursements are paid by the tenant to the landlord to cover some or all of the operating expenses for a property.

- The reimbursement line items on a proforma show what the expected reimbursement amount is for all tenants based on the forecasted operating expenses.

- Depending on the lease, these reimbursement structures can range from simple to surprisingly complex.

- Leases are often categorized as gross leases, modified gross leases, or net leases. Gross leases mean the landlord is responsible for paying all operating expenses for the property. Net leases mean the tenants are responsible for paying all operating expenses. Modified gross leases require both the landlord and the tenant to each pay for a portion of the operating expenses. However, to truly understand who is responsible for paying what, it is important to always read the lease.

Other Income

- Other income is other ancillary income generated by the property. For example, this could include vending, laundry, parking, event income, etc.

- Other income can be either fixed or variable. A fixed amount means that it does not change with the occupancy of the property. An example of a fixed other income item might be income collected from leasing out a billboard or an antenna on the property.

- This contrasts with a variable income item, which does change with the occupancy of the property. For example, parking income or laundry income might change depending on how many tenants occupy the property. Variable income items will be higher as the occupancy of a property increases, and lower as occupancy decreases.

- Other income items will include a percentage to indicate how much of that particular income item is fixed. For example, an ancillary income item that is 100% fixed will not vary at all with the occupancy of a property. An ancillary income item that is 0% fixed will completely vary with the occupancy of the property (in other words, it is 100% variable). And an ancillary income item that is 50% fixed would only partially vary with occupancy.

- Analyzing existing operating statements for a property can help when estimating how much of an ancillary income item is fixed vs variable.

Total Gross Income

- This is the gross income from a property after accounting for actual vacancies, concessions, reimbursements, and all other income.

- This shows the gross income a landlord or owner can expect to generate, before considering any general vacancy or credit loss deductions.

General Vacancy

- The general vacancy factor is a deduction against income to account for vacancy in the property.

- This is often expressed as a percentage of Total Gross Income, but could also be based on other income line items depending on the situation.

- If a lease by lease analysis is completed for all existing leases in place and speculative leases are created for all vacant space, then the general vacancy factor is often not considered at all. This is because the forecast already includes absorption and turnover vacancy which is based on actual leases in place, as well as estimates for leasing up vacant space and re-leasing space for tenants who vacate the property.

- Sometimes a general vacancy factor could still be used as an additional contingency over and above the actual absorption and turnover vacancy. This is often used to ensure the property is in line with the overall market vacancy rate. For example, if you know that the market vacancy rate is 10%, then you may want to include this as a minimum vacancy rate for the property.

- This is accomplished by first taking Total Gross Income and then adding back any Absorption and Turnover Vacancy. This is added back because we don’t want to double count it when applying a general vacancy factor against the total income.

- Then the General Vacancy rate is multiplied by this total income (with the add back) which gives you the amount of general vacancy calculated using only the general vacancy rate and not considering any absorption and turnover vacancy.

- The actual absorption and turnover vacancy is then deducted from the calculated general vacancy amount. If the result is less than 0 then only the absorption and turnover vacancy is shown on the proforma because that means the actual vacancy for the property is higher than the minimum general vacancy factor.

- If the result exceeds 0, then this result (general vacancy minus absorption and turnover vacancy) is shown on the proforma because that means the actual vacancy for the property was not as high as the general vacancy factor.

- This ensures that the proforma always shows vacancy at the greater of actual vacancy projected (absorption and turnover), or the desired general vacancy factor.

- Since these calculations can get tedious and hard to understand in an Excel model, commercial real estate analysis software is typically used for this kind of analysis.

Credit Loss

- Credit loss is a deduction to account for any tenant who does not pay their rent.

- This is often expressed as a percentage of Total Gross Income.

- This can often be estimated based on the historical operating statements for a property.

Effective Gross Income (EGI)

- The Effective Gross Income is the Total Gross Income for a property minus the General Vacancy and Credit Loss estimates.

- This shows the gross income a landlord or owner can expect to receive from a property.

- Property management fees will often be based on the Effective Gross Income because if the property manager can decrease the vacancy, credit loss, and concessions, then their management fee will be higher.

Operating Expenses

- Operating expenses for a property fall into two categories: fixed and variable.

- Fixed expenses are expenses that do not vary with the occupancy of the property. For example, these could include property taxes and insurance expenses because these will be the same, no matter how many tenants occupy the property.

- Variable expenses are expenses that vary with the occupancy of the property. For example, these could include janitorial or utility costs, since more cleaning and more energy will be required as occupancy increases.

- Operating expenses will include a percentage to indicate how much of that particular expense is fixed. For example, an expense that is 100% fixed will not vary at all with the occupancy of a property. An expense that is 0% fixed will completely vary with the occupancy of the property (in other words, it is 100% variable). An expense that is 50% fixed would only partially vary with occupancy.

- The amount of an operating expense as well as how much it varies can be estimated by looking at the historical operating statements for an existing property over the trailing 12 or 24 months.

Net Operating Income (NOI)

- Net Operating Income is the Effective Gross Income for a property, minus any operating expenses. It represents the operating cash flow for the property.

- Net Operating Income is a widely used metric in commercial real estate valuation.

Capital Expenditures

- Capital expenditures are expenditures used to improve the condition of the property itself. Capital expenditures could include a roof replacement, parking lot resurfacing, new HVAC units, etc.

- Capital expenditures differ from operating expenses because they are not required on an ongoing basis for the property to operate.

- Often there will be a Reserves for Replacement line item that is an amount of money set aside to pay for future capital expenditures.

- There is some debate about whether reserves for replacement should be included in Net Operating Income by commercial real estate professionals.

Debt Service

- Debt service or payments for loans used to finance the property are deducted below Net Operating Income.

- This deduction occurs below NOI because it represents an owner-specific expense and not a property level expense. Since different owners have different lender relationships, net worths, income, etc. that means some owners will be able to secure more favorable financing than others.

Cash Flow Before Tax

- This is the bottom-line cash flow an owner of a property can expect to collect before any deductions for taxes.

- While there are many tax benefits to owning commercial real estate, most analysis stops at cash flow before tax due to the complexities of accurately calculating tax liabilities for individual owners in a property. For now, this is outside the scope of this article.

Summary

The detailed proforma for an office, retail, or industrial property follows a similar structure to a simple proforma but includes additional line items and calculations. Potential Rental Income is calculated on a “lease by lease” basis, considering factors such as rent increases, reimbursement structures, and market leasing assumptions. Deductions for absorption and turnover vacancy, free rent, general vacancy, and credit loss are applied to determine the Effective Gross Income. Operating expenses, both fixed and variable, are subtracted from the Effective Gross Income to calculate the Net Operating Income (NOI), a widely used metric in commercial real estate valuation. Further deductions for capital expenditures and debt service result in the Cash Flow Before Tax.

Conclusion

In this article, we defined the real estate proforma, discussed the basic structure of a simple real estate proforma, looked at an example of a single year proforma and also a multi-year proforma, and then walked through a more complicated example of a lease by lease commercial real estate forecast.