The concept of highest and best use is one of the fundamental principles that underlie real estate appraisal. Highest and best use requires that the appraisal considers not just the current use of the property but also the potential value associated with alternative uses. The Appraisal Institute has four tests that appraisers can use in order to narrow down all of the alternatives to one highest and best use of the property.

Four Tests for Highest and Best Use

You can use the following four tests to find the highest and best use of a site as if vacant or currently improved.

1. Is the use physically possible?

The first test of highest and best use simply evaluates whether it is possible to use the land in a certain way. Ignoring the zoning and economics of the proposal, consider whether or not the potential use is physically possible. That means the topography, soil type and conditions, lot size and shape, surface and subsurface water, and even weather patterns must make the development possible. So, you probably can’t build a marina in the middle of the desert, a heavy, marble building on soft clay soil, or a building with a 250,000 square foot base on a 200,000 square foot lot. In addition, an appraiser must not only consider the proposed use of the site but also the characteristics of the optimum improvements for that use. This first test, however, is usually the easiest to pass.

2. Is the use legally permitted?

After eliminating any potential uses that are not physically possible, you can move on to the second test. Whether a potential use is legally permissible involves a few different legal considerations. The proposed use must be allowed by zoning regulations. If building in a residential area with restrictive covenants, the proposed improvements must not violate any rules. The proposed use must conform to all applicable building codes and height limits. In addition, the improvements must adhere to any restrictions imposed by easements on the property.

Determining whether a proposed use is legally permitted requires research into the local building regulations and restrictions. Gaining a comprehensive understanding of the applicable legal requirements can be time-consuming, but it is fairly easy to determine whether or not a proposal violates any of these regulations. Concluding whether or not something is legally permissible is a straightforward process. Regulations, however, change over time. An area that was zoned for residential development can be changed to commercial development. Just because a proposed development is not legally permissible does not mean that it will always be that way. In these cases, an appraiser must consider the probability of the legal restriction being changed to allow the proposed development. In these cases, there should be substantial documentation suggesting that the regulation will be changed in order to pass to the third test of highest and best use.

3. Would the use be financially feasible?

To address whether a proposed use is financially feasible, you need to conduct a market analysis and develop proforma cash flow estimates. You’ll need to collect data in order to forecast construction and development expenses, operating expenses, rents, absorption rates, vacancy rates, discount rates, cap rates, and residual values. Once you’ve gathered all of this information, you will estimate the proforma net operating income over your expected holding period. Employing discounted cash flow techniques, you can determine which projects meet your particular investment standards. Discounting cash flows by your cost of capital and computing the net present value, a project is considered financially feasible if the NPV is greater than 0. You can also compute the internal rate of return and compare the property’s return to your acceptable hurdle rate for projects. Only the proposed property uses that meet these criteria for being financially feasible move to the next step of the analysis.

4. Would the use be maximally productive?

The prior steps eliminated proposed uses that were not physically possible, legally permissible, or financially feasible. This final step takes all of the proposed uses that meet these requirements and ranks them in order of value or rate of return. While ranking proposed uses, it is also helpful to consider the risk associated with the proposed use. For example, one proposed use might generate a much higher internal rate of return than all of the other proposed uses. Yet, the reason for the high return may be related to the higher risk of that project. One way to adjust for the risk associated with a proposed use is to apply a discount rate that is commensurate with the level of risk while computing the net present value. In the end, the proposed use with the highest internal rate of return and net present value is the maximally productive use.

Applying Highest and Best Use to an Existing Structure

To illustrate how highest and best use works in practice, consider an old 1920s brick building in the central business district of a small city. Business and residents moved away from the area, and its current use as retail space may no longer be the highest and best use of the property. It is a 15,000 square foot building, and its estimated value as vacant land is $10/sqft, or $150,000.

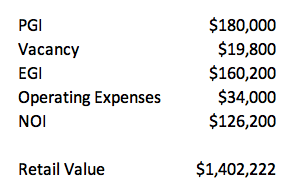

In its current use as retail space, the property generates rent of $12/sqft. Vacancy rates are around 11% since foot traffic generally doesn’t support retail business in the area. Operating costs are $34,000 per year. Since conditions are fairly stable, capitalizing next year’s income at a rate of 9% yields an estimated property value of $1,402,222.

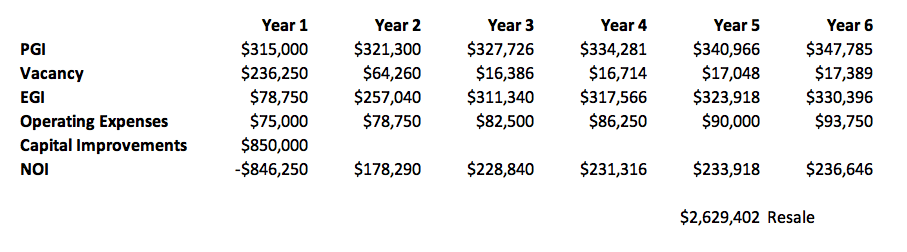

Another alternative would be to renovate the property and convert it into office space. Market research indicates this is a desirable area for professional office such as attorneys, accountants, architects, and designers. Market rent for offices in this area is $21 per square foot and has been increasing by 2% annually. Operating costs average $5/sqft and increase by $0.25 per year. Converting the property into office space will cost $850,000 in the first year, and average vacancy during the year will be 75% due to the time of the renovations. Vacancy is 20% in year 2 and then settles into a constant 5% thereafter. The resale price of $2,629,402 at the end of the 5-year holding period is calculated by dividing year 6 NOI by a 9% cap rate. The net present value of cash flows discounted at a rate of 10% yields a property value of $1,485,848.

Highest and best use analysis evaluates each potential use of the property and its corresponding value. The vacant property is valued at $150,000. Continuing to use the property for retail space yields an estimated value of $1,402,222. Converting the property into office space results in a value of $1,485,848. Highest and best use analysis, therefore, concludes that the best use of the property is as office space.

Conclusion

In this article, we discussed the 4 tests for highest and best use. These 4 tests ask if the proposed use is 1) physically possible, 2) legally permitted, 3) financially feasible, and 4) maximally productive. We then walked through an example of how to apply highest and best use theory to evaluate a property with three potential uses: as vacant land, as an existing structure, and as renovated.