Effective gross income is a line item on a real estate proforma that is commonly used by appraisers, investors, and other commercial real estate professionals. Although the effective gross income is easy to understand conceptually, the calculation itself can sometimes be confusing. In this article, we’ll take a closer look at effective gross income and clear up any confusion.

Effective Gross Income Formula

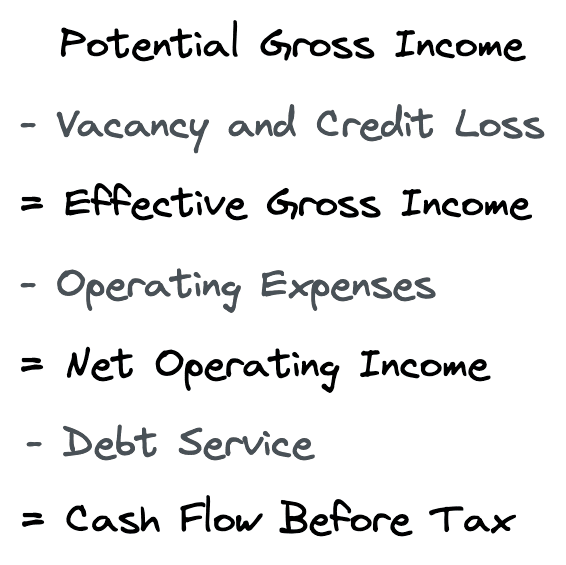

The Effective Gross Income (EGI) formula is defined as the Potential Gross Income for a property minus any vacancy and credit loss.

As you can see in the effective gross income formula above, the effective gross income is an intermediate step when calculating the net operating income and the bottom-line cash flow before tax for a property.

Although the effective gross income calculation can be as simple as the above formula shows, in practice there is often more nuance. Since different commercial properties will have different sources of income, lease structures, reimbursements, etc. that means the effective gross income calculation can vary depending on the property type and circumstances.

How to Calculate Effective Gross Income

Let’s first consider a simple example, and then we’ll look at a more complicated effective gross income calculation.

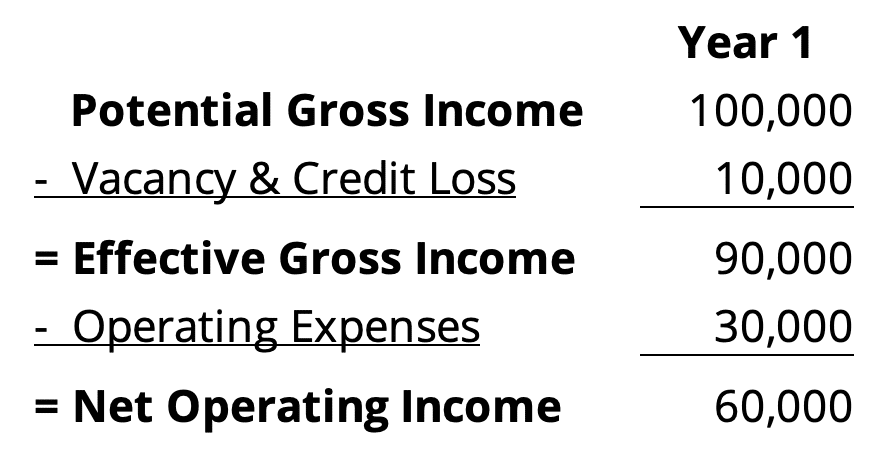

A simple back of the envelope proforma for a single tenant property might look like this:

In this example, the vacancy & credit loss is all shown on one line. In simple proformas like this, the vacancy line item is often calculated using a percentage rate, which is 10% in this case.

The effective gross income above is calculated by taking the potential gross income for the property and subtracting the 10% vacancy and credit loss used. In this example, the effective gross income is 100,000 – 10,000, or 90,000.

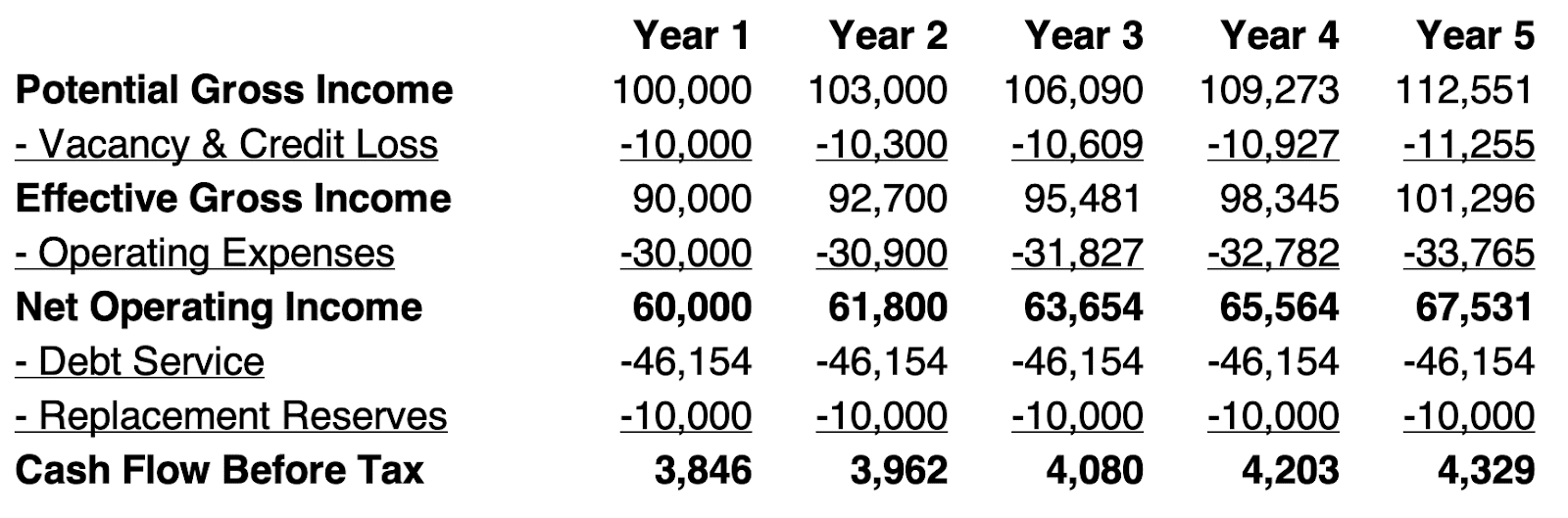

For a multi-period proforma this calculation works the same way and is repeated for each period in the analysis:

Detailed Effective Gross Income Calculation

Since different property types will have different circumstances and characteristics, proforma formats can and do vary in practice. This means the effective gross income calculation itself can vary as well.

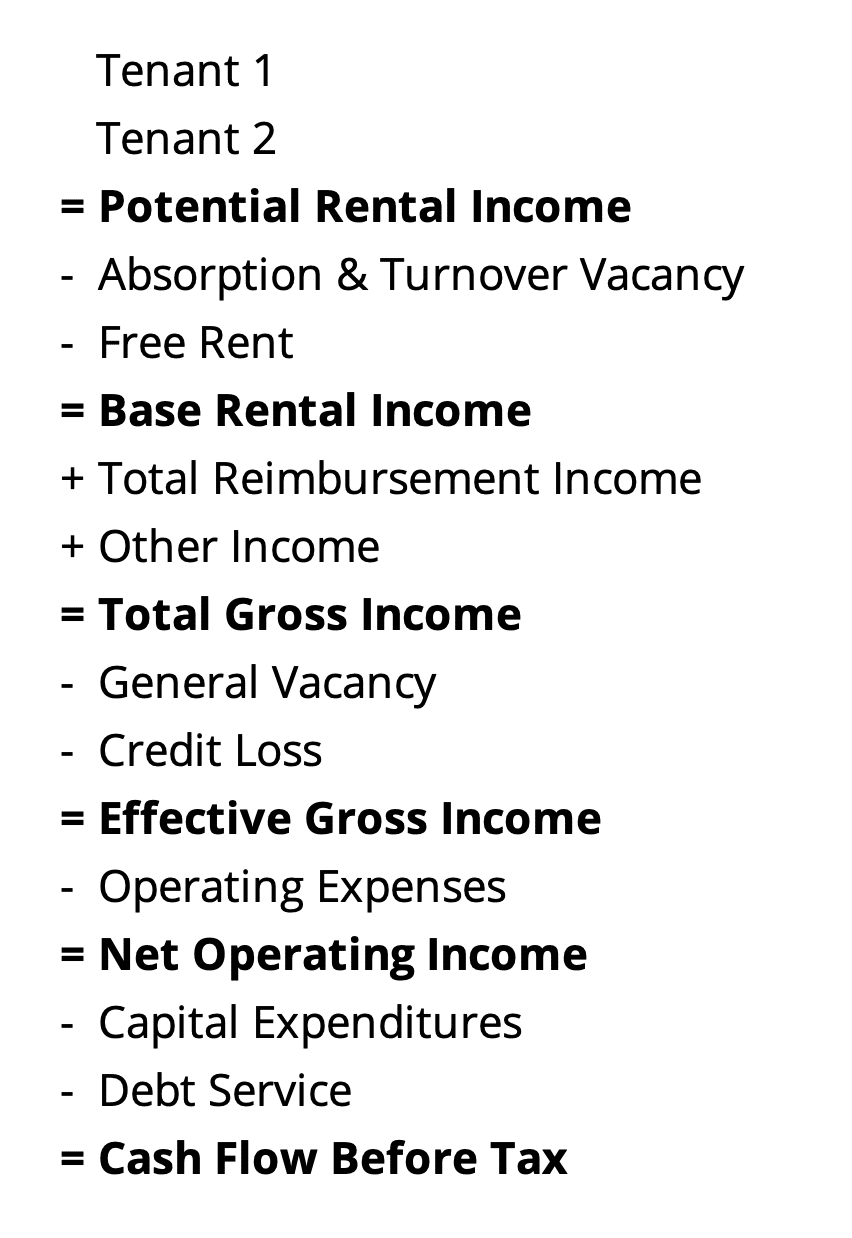

Consider a multi-tenant office building that is half vacant at acquisition, with several leases expiring during the holding period. For a more complicated proforma like this, an absorption and turnover vacancy line item is usually modeled on the proforma. This line item calculates the actual vacancy in the holding period prior to a lease start date (absorption), and the actual vacancy after a lease expires and before the next lease begins (turnover vacancy). This actual vacancy calculation is driven by the tenant’s contractual lease start and end dates rather than an overall percentage vacancy rate like we used in the simple example above. Usually, these market leasing terms are modeled on a proforma using market leasing profiles.

The line items on a more complex proforma might look like this:

To calculate the effective gross income, we start with the potential rental income for the property, which is the base rent a property would earn if it were 100% occupied. For periods of time when a space is vacant, an estimated market-based rent is used to calculate the potential rental income.

Next, we deduct absorption and turnover vacancy. The absorption is equal to the market rent used to calculate potential rental income prior to a lease start date. Likewise, the turnover vacancy is equal to the market rent used to calculate potential rental income after a lease expires prior to the next tenant beginning occupancy. In other words, this absorption and turnover vacancy line item completely offsets any market rent shown during vacant periods in the potential rental income line.

After subtracting any free rent given to tenants as an incentive to sign a new lease, we get to the base rental income line item. The base rental income is the actual base rent a landlord is expected to collect from tenants.

We then add in any reimbursement income from tenants. Reimbursement income calculations can vary from simple to complex, depending on the lease structure for each tenant. For example, a tenant could have a simple triple net lease with an obligation to pay its pro-rata share of all expenses. On the other end of the spectrum is a gross or full service lease that requires the landlord to pay all operating expenses. In this case, there would be no tenant reimbursement. However, a modified gross lease is most common, where both the landlord and the tenant each have some responsibility for paying operating expenses.

Next, we add in any other income for the property which could include parking fees, vending income, etc. This gets us to the total gross income line item, which is the total income a property is expected to generate from tenants as well as other income sources.

We then have a deduction for general vacancy. This is a calculation above and beyond the actual vacancies calculated on the absorption and turnover vacancy line item. This line item is often omitted when using absorption and turnover vacancy calculations. However, sometimes a market vacancy factor is still used in the general vacancy line to ensure the total vacancy in a proforma is at least as high as the market. For example, if the absorption and turnover vacancy amounts to 5%, but the market vacancy rate is 10%, then an extra 5% of vacancy could be shown in the general vacancy line item. It is common for appraisers and lenders to do this when estimating the market value for a property.

A credit loss estimate can also be shown, which is a deduction for tenants who do not pay their rent. This is usually estimated as a percentage of total gross income.

Finally, after deducting general vacancy and credit loss from the total gross income line item, we have calculated the effective gross income.

Effective Gross Income Multiplier

The effective gross income can be used to calculate the gross income multiplier. The gross income multiplier is the ratio of a property’s sale price or value to its gross income.

The effective gross income multiplier uses the effective gross income line item on a proforma as the numerator in the effective gross income formula.

For example, suppose the sales price of a property was 1,000,000, and it had an effective gross income of 200,000. In this case, the effective gross income multiplier would be 1,000,000 / 200,000, or 5.00.

Appraisers sometimes use the effective gross income multiplier along with the net income ratio to estimate the overall capitalization rate. The net income ratio is calculated by taking the net operating income for a property and dividing it by the property’s effective gross income:

This technique is used when strict data requirements can’t be met on comparable sales. If gross income is available for comparable sales then the overall cap rate can still be estimated by using a market average expense ratio which is easier for appraisers to obtain.

For example, suppose the market average expense ratio was known to be 55% for a specific property type in a particular market. A comparable property is identified, but you can only obtain data on potential gross income and effective gross income. In this case, the comparable property sold for 400,000 and had an effective gross income of 80,000. Using this information together with the market average expense ratio, we can estimate the overall capitalization rate.

If we apply the 55% operating expense ratio to the 80,000 effective gross income, then we get an estimated net operating income of 36,000. The effective gross income multiplier is 400,000 / 80,000, or 5.00. The net income ratio is 36,000 / 80,000, or 0.45. Now we can derive the overall capitalization rate from the comparable property as follows:

So, in our example, the overall rate would be 0.45 / 5.00, or 9.0%. This procedure could be repeated for each comparable sale identified. Then an overall capitalization rate could be estimated by reconciling each cap rate derived from the comparables.

Conclusion

In this article, we defined effective gross income, showed you how the effective gross income formula works, and then walked through detailed examples of how to calculate the effective gross income. We used two example calculations. First, we showed you a simple effective gross income calculation that only considers a general vacancy and credit loss factor.

Next, we walked through a more complex example that involved absorption and turnover vacancy, free rent, reimbursement income, and also other miscellaneous income. Finally, we discussed a practical way to use the effective gross income by calculating the gross income multiplier. The gross income multiplier is sometimes used by appraisers to estimate the overall capitalization rate when detailed comparable sales data cannot be obtained.