The capitalization rate, or cap rate, is one of the most important metrics in commercial real estate. It is calculated by dividing a property’s Net Operating Income (NOI) by its value. Commercial real estate professionals use cap rates primarily as a valuation shortcut. It is a way to convert income into property value and compare how the market is pricing similar assets. While it may resemble a return measure, it is not the same as an investor’s actual return. This guide will break down the cap rate formula, provide real-world examples, and address common misconceptions.

Table of Contents

- What is a Cap Rate (Capitalization Rate)?

- How to Calculate Cap Rate: Formula & Steps

- Using Cap Rate for Valuation

- Cap Rate Valuation Example

- Intuition Behind the Cap Rate

- What is a Good Cap Rate?

- When, and When Not, to Use a Cap Rate

- What Determines a Cap Rate? Key Components

- Advanced Cap Rate Calculation Methods

- Cap Rate vs. Discount Rate, IRR, ROI, & Cash on Cash

- Frequently Asked Questions

What is a Cap Rate (Capitalization Rate)?

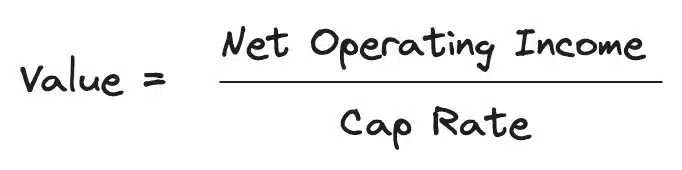

The cap rate (capitalization rate) is a simple formula used in commercial real estate valuation and analysis. It is calculated as the ratio of stabilized Net Operating Income (NOI) to property value:

For example, if a property recently sold for 1,000,000 and had a stabilized NOI of 100,000, then the cap rate would be 100,000/1,000,000, or 10%.

In practice, the cap rate is almost always expressed in terms of an annual stabilized NOI. Because the cap rate is based only on a single year of stabilized NOI, it should be viewed as a pricing shortcut for valuation, not as a measure of an investor’s total return. Actual returns depend on income growth, capital expenditures, financing, and eventual sale.

How to Calculate the Cap Rate: Formula & Steps

There are three simple steps to calculate the cap rate:

- Determine the property’s annual stabilized Net Operating Income (NOI).

- Find the current market value or purchase price of the property.

- Divide NOI by the property value to get the cap rate percentage.

Use our Cap Rate Calculator to quickly estimate a property’s cap rate. For a more detailed analysis, our Proforma App goes beyond quick calculations, allowing you to build customized proformas, model different scenarios, and generate presentation-quality reports.

Using Cap Rate for Valuation

The cap rate is widely used for real estate valuation through direct capitalization. The formula can be rearranged to solve for property value:

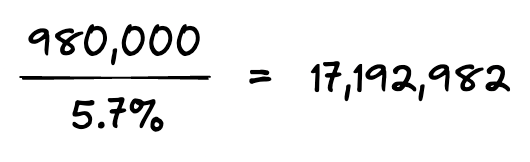

For example, if an investor is analyzing a property with an annual NOI of $980,000 and a market cap rate of 5.7%, the estimated property value would be:

$980,000 / 5.7% = $17,192,982 (rounded to $17,190,000 in practice).

This method provides a quick estimate of property value but assumes a stabilized NOI. If the property’s income is variable, then a discounted cash flow (DCF) analysis is the preferred and often only reliable valuation method.

The cap rate valuation formula is a variation of the perpetuity formula in finance, where the present value of a constant cash flow is determined by dividing it by a discount rate (required rate of return). While real estate cash flows are not truly perpetual, direct capitalization remains a widely used and intuitive valuation method in the industry.

Cap Rate Valuation Example

Let’s take a closer look at how this works. One way an appraiser can estimate the market value of a property is by using the direct capitalization valuation method.

For example, suppose an appraiser is tasked with estimating the market value of a Class A office building that is expected to produce 980,000 in net operating income next year. The appraiser also has data on the following recently sold comparable properties:

Based on the NOI and recent sale prices for each comparable property, we can estimate an average market-based capitalization rate of 5.7%. Using the subject property’s annual NOI of 980,000 and the derived capitalization rate of 5.7%, the appraiser could estimate the property’s market value as:

In practice, this value would usually be rounded down to $17,190,000. While this simplified example doesn’t involve the level of detail and rigor of a formal appraisal, it demonstrates the same fundamental direct capitalization technique used by professional appraisers.

Intuition Behind the Cap Rate

The cap rate is best understood as a valuation shortcut. It is a way to express how much income a property produces relative to its price. In this sense, it works much like the earnings multiple used in stock markets or the current yield on a bond. It’s not a measure of total return but rather a shorthand that lets you compare prices across properties in income terms.

One way to interpret the cap rate is as the amount of annual net operating income a property produces relative to its current market value. A 5% cap rate means a property generates 5 cents in NOI for every dollar invested. A 10% cap rate means it generates 10 cents in NOI for every dollar invested.

Another way to think about it is in terms of payback time. At a 5% cap rate, it takes about 20 years of the stabilized NOI to equal the price you paid. At a 10% cap rate, it only takes 10 years. But it’s important to remember this is a simplified snapshot. Actual investor returns will also depend on future income changes, capital expenditures, financing, and eventual resale.

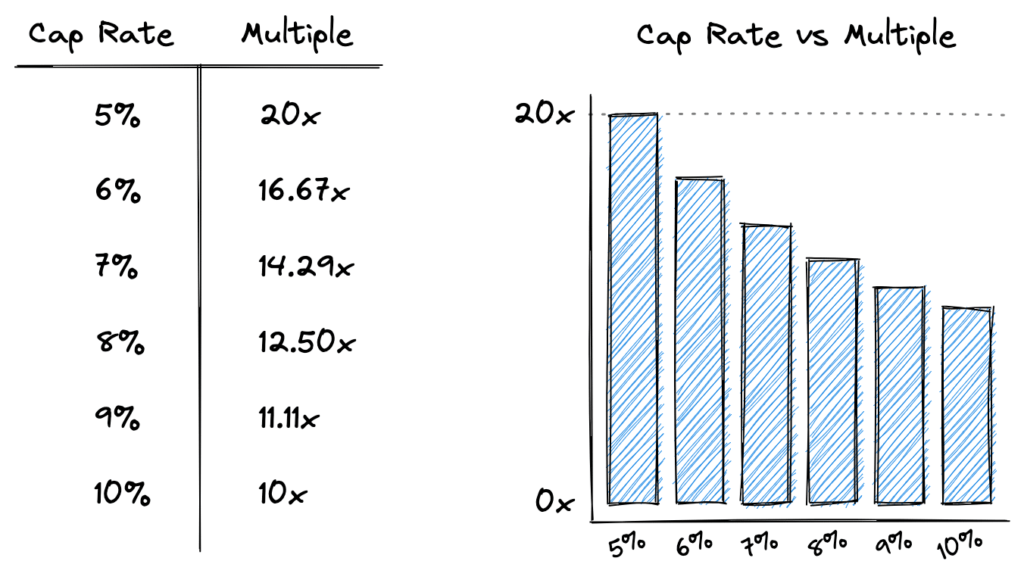

Here’s how you can visualize cap rates as multiples:

As shown in the chart, capitalization rates and NOI multiples are inversely related. In other words, as the cap rate increases, the NOI multiple decreases. That means the higher the cap rate, the shorter the payback time. Investors can use this relationship to quickly assess how a property’s income stream is being valued in the market.

A property’s NOI multiple, calculated as the inverse of its cap rate, indicates how long it takes to recover the purchase price at the stabilized NOI:

NOI Multiple = 1 / Cap Rate

For example:

- 5% cap rate: NOI Multiple = 1 ÷ 0.05 = 20 years

- 10% cap rate: NOI Multiple = 1 ÷ 0.10 = 10 years

Lower cap rates indicate higher property valuations, as investors are willing to pay more for stable, lower-risk income streams.

Because stabilized NOI excludes financing and future changes in income, it’s important to remember that the cap rate is a pricing shortcut, not the total return to the investor. The cap rate itself is not a cause of value. It simply reflects how market participants are valuing property income in light of their opportunity cost of capital, expectations of income growth, and perceptions of risk.

What is a Good Cap Rate?

A “good” cap rate depends on your investment goals, risk tolerance, and market conditions. Sellers typically prefer lower cap rates because they mean higher sale prices, while buyers favor higher cap rates since they imply lower prices relative to income. But even with buyers there is a range depending on investment strategy:

- Conservative Investors: Usually favor lower cap rates in stable markets for predictable returns.

- Opportunistic or Value-Add Investors: Often pursue higher cap rates, betting improvements or market shifts will increase returns.

The best way to judge a cap rate is by comparing it to similar properties in the same market. For instance, if Class A office buildings in your submarket typically trade at a 7% cap rate and you find one at 9%, it’s worth asking why. Is there something wrong with the building (e.g., deferred maintenance, short-term leases, struggling tenants), or is it simply a motivated seller?

In general, prime locations with stable demand usually command lower cap rates because they’re considered safer. Older or more specialized properties (e.g., older hotels, fringe retail) often have higher cap rates to reflect greater uncertainty.

The key point is that there’s no universal “good” cap rate. It’s all about context: property type, location, and strategy. A 6% cap rate might be great for a trophy office building in a big city, but the same number could be too low for a distressed property in a weaker market.

When (and When Not) to Use a Cap Rate

The cap rate is widely used in commercial real estate for quick, initial property valuation and investment comparisons. It’s particularly effective for:

- Comparing Investment Options: Quickly sizing up similar properties. For example, if two similar properties have cap rates of 5% and 10%, the property with the higher cap rate indicates greater risk—but potentially higher returns.

- Analyzing Market Trends: Observing historical cap rate trends can signal market direction. Falling cap rates (“cap rate compression”) suggest rising property values and a competitive market environment.

However, cap rates aren’t suitable for every situation. Specifically, avoid relying solely on cap rates if the property’s NOI is irregular or significantly fluctuates over time. In these cases, a detailed Discounted Cash Flow (DCF) analysis, which accounts for variations in cash flow and the time value of money, provides a more accurate valuation. In these more complex situations, investors commonly use the Internal Rate of Return (IRR), Extended Internal Rate of Return (XIRR), and Net Present Value, which are key outputs of DCF analysis, to measure investment performance.

What Determines a Cap Rate? Key Components

What are the components of the cap rate, and how can they be determined? One way to think about the capitalization rate is that it’s a function of the risk-free rate of return plus some risk premium.

In finance, the risk-free rate is the theoretical rate of return of an investment with no risk of financial loss. Of course, all investments carry some risk in practice. However, since U.S. Treasury bonds are considered to be very safe, the interest rate on a U.S. Treasury bond is normally used as the risk-free rate.

How can we use this concept to determine cap rates?

Suppose you have $10,000,000 to invest, and 10-year treasury bonds are yielding 3% annually. This means you could invest all $10,000,000 into treasuries, considered a very safe investment, and spend your days at the beach collecting checks.

What if you were presented with an opportunity to sell your treasuries and instead invest in a Class A office building with multiple tenants? A quick way to evaluate this potential investment property relative to your safe treasury investment is to compare the cap rate to the yield on the treasury bonds.

Suppose the acquisition cap rate on the investment property was 5%. This means that the risk premium over the risk-free rate is 2%. This 2% risk premium reflects all the additional risk you assume over and above the risk-free treasuries, which considers factors such as:

- Age of the property.

- Creditworthiness of the tenants.

- Diversity of the tenants.

- Length of tenant leases in place.

- Broader supply and demand fundamentals in the market for this particular asset class.

- Underlying economic fundamentals of the region, including population growth, employment growth, and inventory of comparable space on the market.

- Wider societal trends like remote work, AI, etc.

When you break down these components of the cap rate, it reveals their relationship with the risk-free rate and the overall capitalization rate. However, the specific percentages assigned to each risk factor are ultimately subjective and rely on individual business judgment and experience.

Is cashing in your treasuries and investing in an office building at a 5% acquisition cap rate a good decision?

This, of course, depends on how risk-averse you are. An extra 2% yield on your investment may or may not be worth the additional risk inherent in the property. Perhaps you can secure favorable financing terms, and using this leverage, you could increase your return from 5% to 8%. If you are a more aggressive investor, this might be appealing to you. On the other hand, you might want the safety and security that treasuries provide, and a 3% yield is adequate compensation in exchange for this downside protection.

Advanced Cap Rate Calculation Methods

There are some advanced cap rate calculation methods used by appraisers and investors that you should be aware of, most notably the band of investment method and the Gordon model.

Band of Investment Method

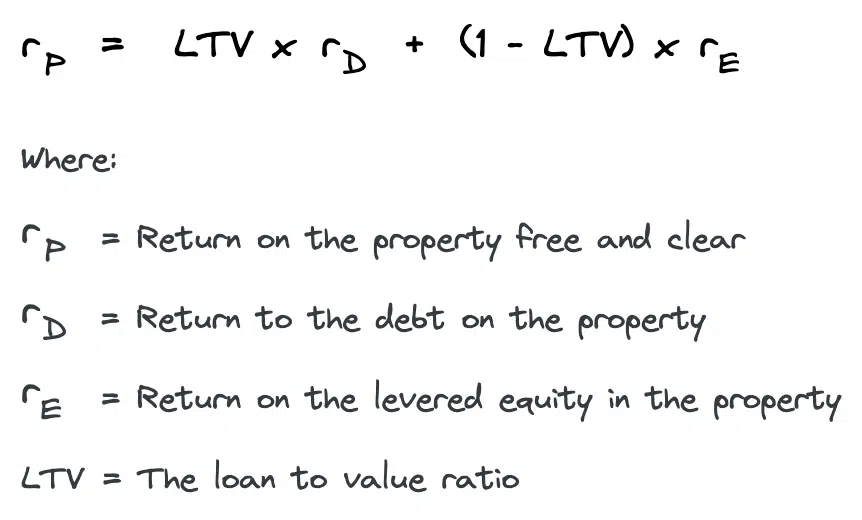

The band of investment method considers returns for both lenders and equity investors. It applies the Weighted Average Cost of Capital (WACC) formula:

The Weighted Average Cost of Capital (WACC) formula is derived from the fact that property cash flow is equal to the sum of cash flow to debt and equity holders. That means if we know two out of the three variables, then the WACC formula can be used to solve for the unknown third component. In other words, when we know the required returns for lenders and investors, then we can calculate the cap rate.

For example, suppose we survey lenders and learn we can secure a loan for a particular property at an 80% Loan to Value (LTV), amortized over 20 years at 6%. This results in a mortgage constant of 0.0859. Further, suppose that a survey of investors reveals the required return on equity is 15%. This results in a weighted average cap rate calculation of 9.87%:

- Loan-to-Value (LTV): 80%

- Loan Constant: 8.59%

- Required Equity Return: 15%

This band of investment calculation is often used by appraisers when comparable sales data is difficult to find. In cases where comparable sales data is sparse or nonexistent, surveys of investors and lenders can provide reliable data to estimate the cap rate using the band of investment methodology.

The Gordon Model

One other approach to calculating the cap rate worth mentioning occurs when NOI isn’t constant but is instead expected to grow at a constant rate. This is the same technique used to value a growing perpetuity. It is also used to value stocks with dividend growth using the dividend discount model, sometimes called the Gordon Model.

If you expect NOI to grow each year at some constant rate, then you can turn this constantly growing stream of cash flows into a simple cap rate approximation.

This formula solves for value, given cash flow, the discount rate, and a constant growth rate. From the definition of the cap rate, we know that value also equals NOI divided by the cap rate.

This means that the capitalization rate can be broken down into two components: the discount rate and the growth rate. That is, the cap rate is simply the discount rate minus the growth rate.

How can we use this? Suppose we are looking at a building with a stabilized NOI of $100,000, and in our analysis, we expect that the NOI will increase by 1% annually. How can we determine the appropriate cap rate to use? Using the Gordon Model, we can simply take our discount rate and subtract out the annual growth rate. If our discount rate (usually the investor’s required rate of return) is 10%, then the appropriate cap rate to use in this example would be 9%, resulting in a valuation of $1,111,111.

The Gordon Model is a useful concept to know when evaluating properties with growing cash flows. However, it’s not a one-size-fits-all solution and has several built-in limitations. For example, what if the growth rate equals the discount rate? This would yield an infinite value, which of course is nonsensical. Alternatively, when the growth rate exceeds the discount rate, then the Gordon Model yields a negative valuation, which is also nonsensical.

These built-in limitations don’t render this technique useless, but you do need to be aware of them. Always make sure you understand the assumptions you are making in an analysis and whether they are reasonable or not.

Cap Rate vs. Discount Rate, IRR, ROI, & Cash on Cash

The cap rate is one of several metrics used to evaluate commercial real estate, and it’s often confused with other return measures. Understanding how it differs from the discount rate, IRR, ROI, and cash-on-cash return will help you use each metric in the right context and avoid common analytical mistakes.

Cap Rate vs. Discount Rate

The cap rate and the discount rate are closely related but not the same thing. The discount rate represents an investor’s required rate of return, or the minimum yield they need to justify taking on the risk of a particular investment. The cap rate, on the other hand, is derived from market transactions and reflects how the market is actually pricing property income.

As covered in the Gordon Model section above, the formal relationship is: Cap Rate = Discount Rate − Growth Rate. This means that when a property’s income is expected to grow, the cap rate will be lower than the discount rate. The gap between the two reflects the market’s expectation for NOI growth.

For example, if an investor requires a 9% return (discount rate) and expects NOI to grow at 2% annually, the implied cap rate is 7%. This is why properties in high-growth markets can trade at cap rates that seem low. The market is pricing in future income increases that the cap rate alone doesn’t show.

The key distinction: the discount rate is forward-looking and reflects an investor’s total required return across all future cash flows. The cap rate is a snapshot based on a single year of stabilized NOI.

Cap Rate vs. IRR

The Internal Rate of Return (IRR) is the most comprehensive return measure in real estate investment analysis. It accounts for the timing and magnitude of all cash flows over a holding period, including operating income, capital expenditures, financing costs, and the eventual sale. It solves for the annualized rate of return that makes the net present value of those cash flows equal to zero.

The cap rate, by contrast, is based on a single year of stabilized NOI and ignores financing, future income changes, capital expenditures, and sale proceeds entirely. Think of it this way: the cap rate tells you how the market is pricing a property’s income today, while the IRR tells you what your actual investment performance looks like over time.

This is precisely why you can have two properties with identical cap rates but very different IRRs. A property purchased at a 7% cap rate in a market with strong rent growth and low capital expenditure needs could produce a 12% IRR, while a 7% cap rate property with flat rents and a major roof replacement ahead might produce only a 6% IRR.

When to use which: cap rates are useful for quick comparisons and initial screening. IRR (via a discounted cash flow analysis) is the appropriate tool for making actual investment decisions.

Cap Rate vs. ROI

Return on Investment (ROI) is a general measure of investment profitability, calculated as the total gain from an investment divided by the total amount invested. In real estate, ROI typically captures everything: rental income, appreciation, tax benefits, and any proceeds from a sale.

The cap rate is much narrower. It uses only stabilized NOI (before debt service, capital expenditures, and taxes) divided by the property’s current market value or purchase price. It also assumes an all-cash purchase, which means financing plays no role in the calculation.

This means the cap rate will almost always differ from an investor’s actual ROI. If you finance the purchase, your cash invested is less than the property’s price, and leverage amplifies both gains and losses. If the property appreciates and you sell at a profit, that shows up in ROI but not in the cap rate. If you spend $200,000 on a new HVAC system, that reduces your ROI but the cap rate doesn’t account for it.

The cap rate is best understood as a market pricing metric, while ROI is a performance metric. One tells you how the market values income; the other tells you how your investment actually did.

Cap Rate vs. Cash-on-Cash Return

Cash-on-cash return measures the annual pre-tax cash flow an investor receives relative to the total cash they invested. The formula is:

Cash-on-Cash Return = Annual Pre-Tax Cash Flow / Total Cash Invested

The critical difference from the cap rate is that cash-on-cash return accounts for financing. After you subtract your annual debt service from NOI, the remaining cash flow is divided by the equity you put into the deal (your down payment plus closing costs and any initial capital improvements).

For example, suppose you buy a property for $2,000,000 with an NOI of $140,000 and a cap rate of 7%. If you finance 75% of the purchase at a 6.5% rate with a 25-year amortization, your annual debt service is approximately $121,000. Your cash-on-cash return would be:

($140,000 − $121,000) / $500,000 = 3.8%

Same property, same 7% cap rate, but only a 3.8% cash-on-cash return because of the financing terms. Conversely, if interest rates were lower or you secured better terms, the same cap rate could yield a much higher cash-on-cash return. This is why investors who use leverage care deeply about both metrics. The cap rate tells them whether the property is fairly priced in the market, and the cash-on-cash return tells them whether the deal works given their specific financing.

Cap Rate vs. Yield

In bond markets and other financial contexts, “yield” typically refers to the total return an investor receives, including both income and price changes. In real estate, the term is used less precisely, which can cause confusion.

The cap rate is sometimes called a “yield,” but it is more accurately described as an income yield. It reflects only the current income relative to price, similar to the current yield on a bond or the dividend yield on a stock. It does not include appreciation, depreciation, or any changes in income over time.

In appraisal practice, the yield rate (also called the discount rate or internal rate of return) is the broader measure that captures total investment return across all cash flows, including income growth and reversion. The cap rate and yield rate are mathematically linked through the Gordon Model relationship covered earlier, but they measure different things. The cap rate is a pricing metric; the yield rate is a return metric.

Quick Comparison Table

| Metric | What It Measures | Accounts for Financing? | Time Horizon | Best Used For |

|---|---|---|---|---|

| Cap Rate | NOI relative to property value | No (assumes all-cash) | Single year (stabilized) | Market pricing comparisons, quick valuation |

| Discount Rate | Investor’s required total return | Depends (unlevered vs. levered) | Multi-year (all future cash flows) | DCF analysis, setting return hurdles |

| IRR | Rate of return across all cash flows | Depends (unlevered vs. levered) | Full holding period | Investment decisions, performance measurement |

| ROI | Total gain relative to total invested | Depends (unlevered vs. levered) | Full holding period | Overall profitability assessment |

| Cash-on-Cash | Annual cash flow relative to equity invested | Yes | Single year | Evaluating leveraged deals, comparing financing scenarios |

| Yield Rate | Total return including income + appreciation | No | Multi-year | Appraisal, DCF discount rate selection |

The cap rate is the simplest metric in this group, and that’s its strength. It strips away financing, holding period assumptions, and income growth to give you a clean, comparable measure of how the market prices property income. But for the same reason, it should never be the only metric you use to make an investment decision. Pair it with a DCF analysis and IRR calculation for a complete picture of any deal.

Cap Rate Cheat Sheet

Fill out the quick form below and we’ll email you our free cap rate Excel cheat sheet containing helpful calculations from this article.

The Many Layers of Valuation

Commercial real estate valuation is a multi-layered process and usually begins with simpler tools than the discounted cash flow analysis. The cap rate is one of these simpler tools that should be in your toolkit. The capitalization rate is widely used and can communicate a lot about a property quickly, but it can also exclude many important factors in a valuation, most notably the impact of irregular cash flows.

The solution is to create a multi-period cash flow projection and discounted cash flow analysis to arrive at a more accurate valuation. If you need help building a cash flow projection and running a discounted cash flow analysis, consider giving our commercial real estate analysis software a try.

Cap Rate: Frequently Asked Questions

A 7.5% cap rate means the property produces $7.50 in annual net operating income for every $100 of property value. On a $2,000,000 property, that translates to $150,000 in annual NOI. It also implies an NOI multiple of about 13.3x, meaning it would take roughly 13.3 years of stabilized NOI to equal the purchase price.

It depends on your perspective. Sellers prefer lower cap rates because they translate to higher property values. Buyers generally prefer higher cap rates because they mean a lower price relative to income. For investors, the “better” cap rate depends on strategy. A lower cap rate usually signals a more stable, lower-risk property, while a higher cap rate often comes with more risk but greater income relative to price.

Cap rate compression occurs when cap rates decline over time, meaning property values are rising relative to NOI. This typically happens during economic expansions when investor demand for real estate is strong, risk premiums are declining, and expectations for future income growth are increasing. The opposite, cap rate expansion, occurs when cap rates rise and property values fall relative to income.

Rising interest rates tend to push cap rates higher because they increase the risk-free rate component of the discount rate. However, the relationship is not one-to-one. When rates rise because the economy is strong, NOI growth expectations may also increase, partially offsetting the effect on cap rates. The net impact depends on all three components of the cap rate: the risk-free rate, the risk premium, and expected income growth.

Cap rates are primarily used for commercial and investment real estate. They can be applied to residential rental properties like duplexes and apartment buildings, but they are not commonly used for owner-occupied single-family homes. Owner-occupied homes don’t produce rental income, so there is no NOI to capitalize. For single-family rentals, cap rates can be useful but should be supplemented with other metrics because the market for these properties is heavily influenced by owner-occupant demand, not just investor pricing.

The terminal cap rate (also called an exit cap rate or reversion cap rate) is the cap rate used to estimate a property’s sale price at the end of a holding period in a discounted cash flow (DCF) analysis. It is applied to the projected NOI in the year following the sale. Terminal cap rates are typically set slightly higher than the going-in cap rate to account for the aging of the property and the uncertainty of projecting income further into the future.

The cap rate measures a single year of stabilized NOI relative to property value and assumes an all-cash purchase. ROI is broader and can account for financing, capital expenditures, appreciation, tax benefits, and sale proceeds over the entire holding period. The cap rate is a market pricing metric that helps you compare how properties are valued. ROI is a performance metric that measures how your investment actually performed. For a detailed breakdown, see our cap rate vs. ROI comparison above.

NOI is the numerator in the cap rate formula (Cap Rate = NOI / Property Value), so changes in NOI directly affect the cap rate when the property value stays the same. If NOI increases while the purchase price remains constant, the cap rate goes up. If NOI decreases, the cap rate goes down. This is why it matters which NOI figure you use. Trailing 12-month NOI, forward 12-month NOI, and stabilized NOI can all produce different cap rates for the same property, especially during market transitions.

There is no standard cap rate for Airbnb properties because short-term rental income is more volatile than traditional leases. A cap rate of 8% to 12% is common for short-term rental investments, but the NOI is harder to stabilize. Revenue depends heavily on occupancy, seasonal demand, local regulations, and platform fees. Because of this income variability, many investors supplement cap rate analysis with a full discounted cash flow (DCF) analysis when evaluating short-term rental properties.

Conclusion

In this article, we defined the cap rate, walked through an example of how an appraiser uses the capitalization rate to estimate the market value of a property, and then we looked at the intuition behind the calculations. Next we covered what a good cap rate is, when not to use a cap rate, and discussed how to think about the components of the cap rate. Finally, we discussed the band of investment method and Gordon model as practical ways to calculate the capitalization rate when you have limited information or growing cash flows.