More often than not, some portion of every commercial real estate transaction is financed with debt. Typically, that debt comes from a bank or non-bank lender who agrees to lend a certain amount of money in return for certain concessions from a borrower. For example, they will almost always require a 1st position mortgage on the property securing the loan and could require the borrower to agree to certain covenants around Debt Service Coverage or Loan to Value.

Depending on the lender, they may also require the personal guarantee of the borrower(s)/sponsor(s) in the transaction.

What is a Personal Guarantee?

In a typical commercial real estate transaction, a lender will look for three sources of repayment. In most cases, it looks something like this:

- Primary Source of Repayment: Cash flow from property

- Secondary Source of Repayment: Sale of property

- Tertiary Source of Repayment: Execution of personal guarantee

This structure means that the bank will first evaluate the financial strength of the property to ensure that it produces enough cash to make the monthly loan payments. As long as this is the case, there are no issues. As a backup plan, they will also analyze the value of the property to ensure it could be sold for enough money to repay the outstanding loan balance. As a last resort, if the property sale price is not enough to repay the loan balance, the lender will turn to the transaction sponsor who must reach into their own pocket to make up the difference, To illustrate how this works, consider the following example.

Suppose that borrower has defaulted on a loan with an outstanding balance of $1,000,000. This means that the primary source of repayment has failed. As such, the lender turns to the secondary source by foreclosing on the property and selling it for $900,000. These funds are applied to the loan balance, but there is still $100,000 outstanding. When the bank executes on the personal guarantee, it means that the sponsor(s) would have to reach into their own pockets for the $100,000 needed to repay the loan in full.

Relying on guarantor resources for repayment underscores the need for the lender to understand exactly what they look like. The primary way this is accomplished is through requiring each one of them to complete a Personal Financial Statement.

Evaluating Sponsor Financial Strength – The Personal Financial Statement

A Personal Financial Statement is an individual balance sheet that lists each guarantor’s income, assets, and liabilities. Lenders use it to evaluate the financial situation of each “guarantor” / endorser and the collective strength of multiple guarantors. The specific template or form used to create a personal financial statement varies by lender, but they all contain the same general information, which is discussed in detail below.

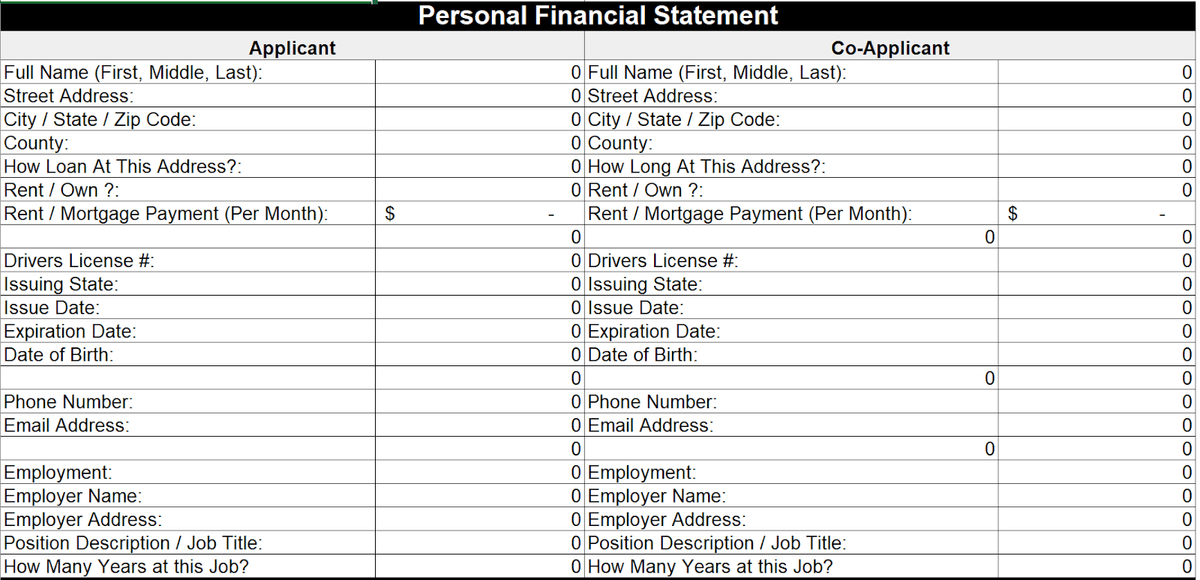

Personal Information

The first section is fairly straightforward and it contains personal information about the individual or couple that is completing the Personal Financial Information. Typically it includes some combination of the following:

- Name

- Address

- Length of time at current address

- Rent or own primary residence

- Drivers License Information

- Employment information such as employer, title, and length of time in the current role.

The intent of this information is to identify who the guarantor is, where they live, and what they do for work. When pulling a credit report, this information can be cross referenced to ensure the credit report has been pulled on the right person(s). An example of this section is shown in the screenshot below:

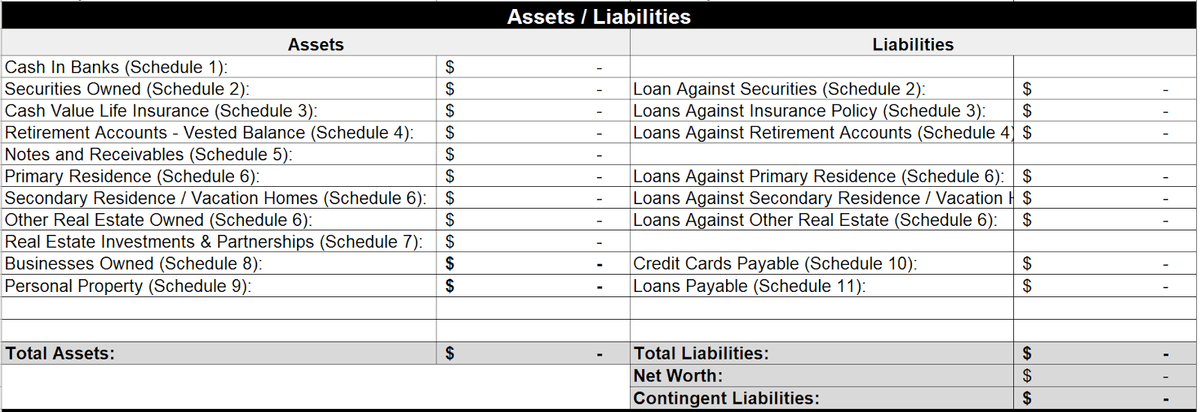

Assets & Liabilities

This is the key section of the Personal Financial Statement. It is where the individual(s) completing it list their personal assets and liabilities. When the lender reviews this section of the PFS, they are looking for the following key information:

- Liquidity: This may be the most important number on the Personal Financial Statement. Typically, liquidity includes: cash, savings accounts, checking accounts, mutual funds, certificates of deposit, cash surrender value of life insurance, money market accounts, marketable securities, and any other asset that can be converted to cash quickly.

As a general rule of thumb, lenders want to see liquidity equal to 10% of the loan amount, after the down payment has been made. For example, a $1,000,000 loan would require $100,000 in liquidity.

- Total Assets: Non-liquid assets include: primary and secondary residences, real estate partnerships, retirement accounts (401k, IRA, etc.), businesses ownership interests, and personal property like collectibles, notes receivable, jewelry, household goods, and automobiles.

The listed value of non-liquid assets is typically taken with a grain of salt by the lender as borrowers are notorious for overstating their value and they would be unlikely to fetch full price in a liquidation scenario. For example, if a car is listed as being worth $25,000 and the borrower had to sell it under duress, they may only get $18,000 or $20,000.

- Liabilities: Total liabilities can be thought of in two groups, short term and long term. Short term liabilities are those that are due in less than 12 months and they include things like credit card balances, unpaid taxes, and payday loans. Long term liabilities are those due in more than 12 months and they include account balances for things like: car loans, personal loans, business loans, and mortgages payable.

From an analysis standpoint, a lender typically compares the combined outstanding balance of short term liabilities to the individual’s liquidity to ensure there is enough cash on hand to cover them. For example, if an individual has $25,000 in liquidity, but $50,000 in short term liabilities, this could be potentially problematic.

- Contingent Liabilities: Contingent Liabilities are often overlooked, but critically important. They represent other loans that the sponsors have guaranteed. They are important because, if the borrower defaults on one of the other loans, their ability to support the subject loan could be impaired.

Typically, contingent liabilities are categorized according to the likelihood that the individual will have to support them. The categories are:

- Realizable: A loan that has a high likelihood of default, meaning the individual may have to support it. These would include loans that are already delinquent or for which payments have been missed.

- Potentially Realizable: A loan that may default or one that has the potential for requiring a borrower’s support. This bucket typically includes loans for land or development projects since they tend to be the highest risk.

- Potentially Unrealizable: A loan that is lower risk that the borrower may have to support at some point in the future. These could include loans for properties that aren’t currently cash flowing or ones for which covenants have not been met.

- Unrealizable: A loan which is unlikely to ever need support by the individual providing the PFS. These typically include loans for cash flowing properties and those that have a long history of performing as agreed.

If the realizable or potentially realizable contingent liabilities are significantly larger than an individual’s liquidity or total assets, it could be problematic for the lender because it means that the individual’s assets could be wiped out by a different loan.

An example of the Assets/Liabilities section is below:

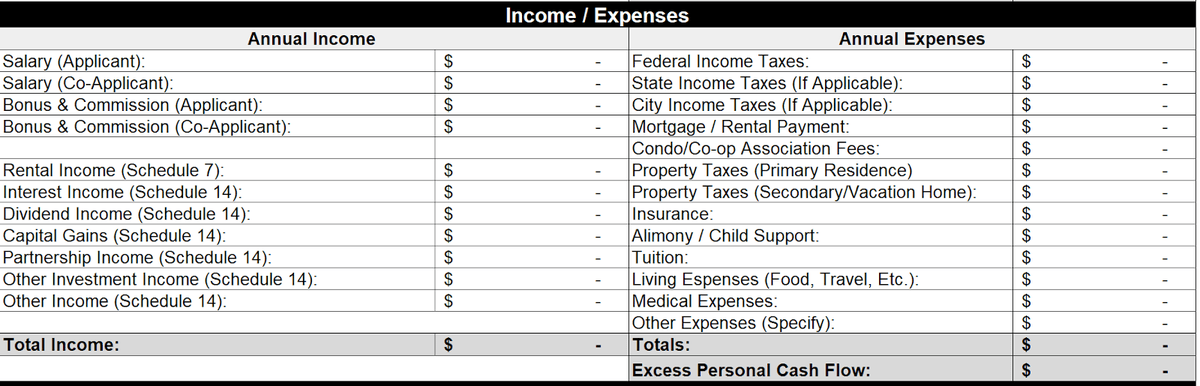

Income / Expenses

The next most important element of an individual’s financial condition is how much money they earn and spend in a given month. This is shown on the income statement portion of the PFS.

Annual income is derived from a variety of sources including employment, alimony, interest, dividends, and K-1 distributions. Income in and of itself is not a critically important metric, but net income is. A sponsor may have a high income, but if they also have high expenses, their net income may not be sufficient to support the loan’s payments in a worst case scenario.

Expenses consist of everyday living expenses for things like food, travel, child support, and housing. They also include debt service for things like mortgage payments, student loans, payments for existing loans like mortgages and car notes.

An example of the income/expenses section is shown in the screenshot below:

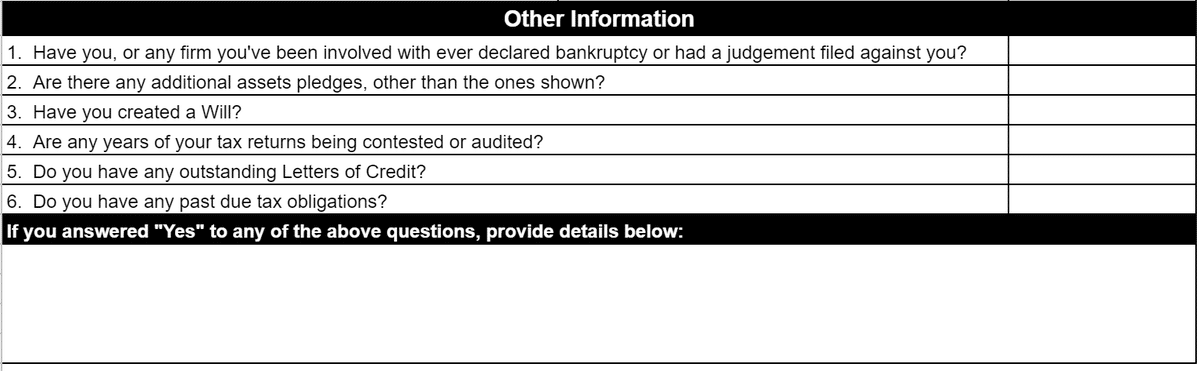

Other Information

Finally, there may be an “other information” section that contains a series of questions about the borrower’s personal history. The point of the questions is to cover a few key items that wouldn’t be captured in the asset, liability, and income numbers provided by the borrower. In the PFS template that we use, these questions include:

- Have you ever declared bankruptcy?

- Are your assets pledged anywhere else?

- Have you created a will?

- Are your tax returns being audited?

- Do you have any outstanding Letters of Credit?

- Do you have any past due tax obligations?

If the answer to any of the above questions is yes, then it is likely that the lender will ask the guarantor to provide more information about the situation. For example, if it turns out that the guarantor’s tax returns are being audited by the IRS, they may have to pay a tax penalty which would have to be subtracted from their available liquidity. A yes to any of the questions does not necessarily disqualify the borrower, but it does indicate a need for further investigation.

A screenshot of the “Other Information” section is provided below:

Summary & Conclusions

As a part of the commercial loan approval process, a financial institution or commercial real estate lender will require their borrower(s) to complete a Personal Financial Statement.

A Personal Financial Statement is a listing of the income, assets, and liabilities of each guarantor and they are used by the lender as a way to analyze the tertiary source or repayment in a loan transaction. The format of the PFS often varies from one lender to another, but they all contain the same general information and share the same general goal of summarizing the guarantor’s financial position.

The Assets sections lists all of the things of value that the guarantor owns and they are divided into short and long term categories. Short term assets include things like cash, money market accounts, and marketable securities. Long term assets include things like cars, houses, and collectibles. They are listed at market value.

The Liabilities section is also divided into short and long term categories. Short term liabilities include things like credit card debt and payday loans. Long term liabilities include things like mortgages, car loans and income taxes payable.

Finally, the income lists the borrower’s sources of income. Typically they include categories like: wages, dividends, interest, distributions, and gifts.

The higher the net worth and liquidity of the guarantor(s), the more support they bring to the loan request and the more likely it is to be approved. If the guarantor(s) have a negative net worth, it subtracts from the transaction and could be a reason to decline it.