Market leasing assumptions define what happens after a tenant lease expires in a commercial property. Since it’s unknown whether the tenant will renew its lease or not, there are two sets of assumptions. One set of assumptions is used if a new tenant needs to be found. The second set of assumptions is used if an existing tenant renews its lease. Then, there is a renewal probability that creates a weighted average between these two sets of assumptions.

At a high level, the concept of market leasing assumptions is easy to understand. However, with multiple leases, complex assumptions, and various levels of uncertainty, even seasoned commercial real estate professionals can get stuck or confused. In this article, we’ll take a deep dive into market leasing assumptions, dispel some common misconceptions, and then tie it all together with some relevant examples.

Market Leasing Assumptions: Office Building Example Part 1

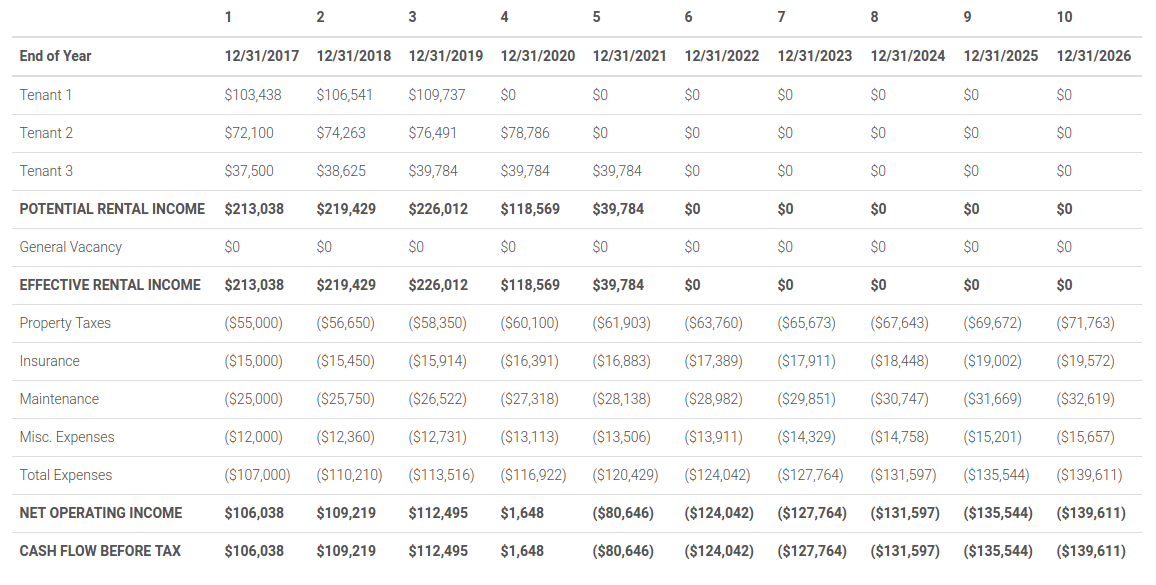

To motivate our discussion, let’s start with a simple case study for an office building analysis. Suppose we have a 15,000 square foot building with an analysis start date of January 1st, 2017 and the following rent roll:

There is a large tenant occupying 7,500 square feet, a medium sized tenant occupying 5,000 square feet, and small tenant occupying 2,500 square feet. The large tenant’s lease expires in 3 years on December 31st, 2019. The medium sized tenant’s lease expires a year later on December 31st 2020. And the small tenant’s lease expires one more year later on December 31st, 2021. The first two tenants have annual rent escalations of 3%. The third tenant also has annual rent escalations of 3%, but only for the second and third years of its lease. To keep things simple, there are no reimbursements, leasing commissions, or tenant improvements.

For our expenses we will assume the following:

- Property Taxes are $55,000 per year with 3% annual escalations

- Insurance is $15,000 per year with 3% annual escalations

- Maintenance is $25,000 per year with 3% annual escalations

- Miscellaneous expenses are $12,000 per year with 3% annual escalations

So, based on the above assumptions, this is what a first draft 10 year proforma looks like with an analysis start date of January 1st, 2017:

As you can see, starting in year 4, there is a significant amount of lease rollover risk with this property. We have one lease expiring in year 4, another in year 5, and yet another in year 6. What happens after these leases expire and how do we account for this in our analysis? Let’s take a closer look at how market leasing assumptions can help.

How Market Leasing Assumptions Work

Before we complete our analysis above, let’s first take a closer look at how market leasing assumptions work. There are two possibilities after a lease expires: 1) the tenant vacates and you have to re-lease the space at the then prevailing market rents and terms, or 2) the tenant renews its lease, possibly at rent and terms different than the market.

Since it’s unknown which of these two outcomes will occur (vacate or renew), “market leasing assumptions” take into account both outcomes. Both scenarios are taken into account by calculating a weighted average between the two outcomes based on a “renewal probability” you enter, which is just your best guess on a scale of 1-100 of the chance a tenant will renew its lease. This results in a blended market/renewal calculation that is ultimately used in the proforma cash flows to account for the uncertainty of tenant renewal.

For example, if you enter a 100% renewal probability then all market inputs will be ignored and only the renewal inputs will be used in the analysis. Likewise, if you enter a 0% renewal probability, then it’s assumed the tenant will certainly NOT renew its lease and therefore all renewal inputs will be ignored and only market inputs will be used.

If you aren’t certain that the tenant will renew or vacate, then you can enter a renewal probability somewhere between 0% and 100%, and the market leasing assumptions will calculate a weighted average between the two possible outcomes. Let’s take a closer look at how this works.

For example, suppose you believe there is a 50% chance the tenant will renew its lease. In either case, here are the market rent/terms and renewal rent/terms:

| Market | Renewal | Blended (50%) | |

| Rent | $10/SF | $9/SF | $9.50/SF |

| Leasing Commissions | 5% | 0% | 2.5% |

| Tenant Improvements | $25,000 | $5,000 | $15,000 |

| Free Rent | 6 months | 0 months | 3 months |

| Months Vacant | 3 months | 0 months | 1.5 months |

As you can see in the above table, the market rent and terms are different than the renewal rent and terms. The renewal assumptions are often at a discount to the market assumptions because renewing a tenant already in place is less costly. To account for this, as well as the 50% possibility that the tenant vacates, the market leasing assumptions create a weighted average between the market and the renewal assumptions. In this case each set of assumptions is weighted equally at 50%, and the result is shown in the “Blended” column above. Let’s take a quick look at each of the line items above, plus some additional market leasing assumptions.

Weighted Inputs

Rent – This is simply the base rent expected for either a new tenant at the market rate, or an existing tenant renewing its lease.

Leasing Commissions – This is the leasing commission paid to find a new tenant at the market rate, or to renew an existing tenant lease.

Tenant Improvements – This is an amount provided by the landlord to the tenant for improvements to the tenants space.

Free Rent – This is the abatement or free rent concession sometimes used to attract a new tenant.

Months Vacant – This defines the downtime after a lease expires if you need to go to the market to find a new tenant. There is no Renewal input for months vacant because if a tenant renews its lease there is by definition no downtime.

Non-Weighted Inputs

In addition to the above weighted inputs, there are also several non-weighted market inputs commonly used. These non-weighted inputs are not affected by the renewal probability. Let’s take a quick look at the non-weighted market leasing assumptions.

Market Lease Term – Once the market/renewal lease begins, the market term defines how long the market/renewal lease lasts in years. This will also affect the timing of the market/renewal leasing commission, tenant improvements, and rent increases that occur within market term itself. After a market term expires all market leasing assumptions reset for the next market term.

Rent Increases – This is the annual rent escalation applied over the market lease term. This will apply to the blended market/renewal and is based on the market term.

Market Inflation – The general market inflation factor is applied to all market and renewal rent entered. The market and renewal inputs are as of the analysis start date and any market inflation entered will apply each year on the anniversary of the analysis start date. When a lease expires, market leasing assumptions will automatically calculate the then prevailing market/renewal rent, which will include any market inflation up to that point in time. This is not to be confused with market rent increases, which simply define the annual escalation factor inside of a market lease term.

Market Reimbursements – The market reimbursements work just like lease reimbursements and will apply no matter what renewal probability is entered.

Now that we’ve covered how market leasing assumptions work, let’s apply some market leasing assumptions to our office building case study to complete our analysis.

Market Leasing Assumptions: Office Building Example Part 2

Now that we’ve covered how market leasing assumptions work, let’s wrap up our office building analysis from above. Suppose we have the following 3 sets of market leasing assumptions, one for each tenant:

Large Sized Tenant Market Leasing Assumptions (Tenant 1)

| Market | Renewal | Blended (50% renewal probability) | |

| Rent | $14/SF | $12.60/SF (10% discount) | $13.30/SF |

| Leasing Commissions | 5% | 0% | 2.5% |

| Tenant Improvements | $25,000 | $0 | $12,500 |

| Free Rent | 6 months | 0 months | 3 months |

| Months Vacant (Downtime) | 0 months | 0 months | 0 months |

Medium Sized Tenant Market Leasing Assumptions (Tenant 2)

| Market | Renewal | Blended (75% renewal probability) | |

| Rent | $14.50/SF | $13.05/SF (10% discount) | $13.41/SF |

| Leasing Commissions | 5% | 0% | 1.25% |

| Tenant Improvements | $20,000 | $0 | $5,000 |

| Free Rent | 6 months | 0 months | 1.5 months |

| Months Vacant | 0 months | 0 months | 0 months |

Small Sized Tenant Market Leasing Assumptions (Tenant 3)

| Market | Renewal | Blended (25% renewal probability) | |

| Rent | $15/SF | $13.50/SF (10% discount) | $14.63/SF |

| Leasing Commissions | 5% | 0% | 3.75% |

| Tenant Improvements | $10,000 | $0 | $7,500 |

| Free Rent | 6 months | 0 months | 4.5 months |

| Months Vacant | 4 months | 0 months | 3 months |

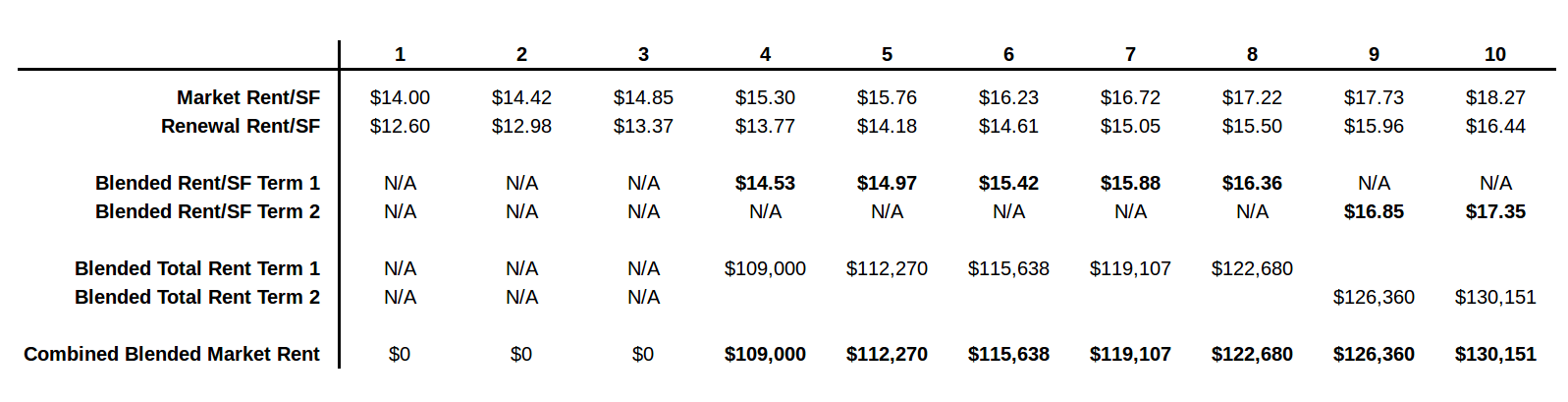

To keep things simple, let’s assume for all 3 tenants that there are no market reimbursements and that all market terms are 5 years. However, we will assume a market inflation factor of 3% for all three tenants as well as 3% rent increases during the market term.

Recall that the difference between the market inflation factor and the market rent increases is that the rent increases apply during the market term while the general market inflation factor is applied to market/renewal rent, which is inputted as of the analysis start date. What happens at lease expiration is the then prevailing market and renewal rent (which could be inflated at the market inflation factor) is calculated and used in the weighted average market/renewal rent calculation. Then, this resulting blended rent calculation is used at the start of market lease term. And during the market lease term the market rent increases will apply each year. Finally, at the expiration of the market lease term this process simply repeats itself.

If this is confusing don’t worry. Let’s break this down step by step. Here’s what the market rent calculations look like for Tenant 1.

Market Leasing Calculations for Tenant 1

Remember that the above market and renewal rent inputs are as of the analysis start date. So, for Tenant 1, a market rent of $14/SF as of the analysis start date with 3% annual market inflation would be a market rent of $15.30 in year 4 . Likewise the renewal rent in year 4 would be $13.77. These calculations are shown in the above table on the first two rows.

Remember that the above market and renewal rent inputs are as of the analysis start date. So, for Tenant 1, a market rent of $14/SF as of the analysis start date with 3% annual market inflation would be a market rent of $15.30 in year 4 . Likewise the renewal rent in year 4 would be $13.77. These calculations are shown in the above table on the first two rows.

The next two rows show the blended market rent for each market term over the holding period. This simply takes a weighted average of the first two lines we calculated above using the renewal probability. Since our renewal probability for Tenant 1 is 50%, the first Blended Rent/SF Term 1 line shows $14.53 per square foot in year 4, which is just (50% x $15.30 + 50% x $13.77). Since our market/renewal lease begins on the first day of year 4, our market rent is $14.53 for the entire year. Then in year 5 our market rent is escalated by the Market Rent Increase assumption of 3%, which results in a market rent per square foot of $15.42. This continues for the entire 5 year market lease term which ends in year 8. This first 5 year market/renewal term is shown in bold above on line 3.

At the end of year 8 our first market terms ends, and in year 9 our second market term begins. At this point in time we need to first figure out what the then prevailing market/renewal rent is, which again, is shown on the first two rows of the table. In this case we can see that our market rent in year 9 is $17.73 and our renewal rent in year 9 is $15.96. And the blended rent assuming a 50% renewal probability is $16.85. This is shown in year 9 for the Blended Rent/SF Term 2 line item. Since we are now in the second market lease term, this starting blended rent is escalated in year 10 by the 3% Market Rent Increase. This process continues for all 5 years of the second market lease term. However, since our analysis period is only 10 years long, only the first two years of the second market lease term are shown.

Proforma With Market Leasing Assumptions

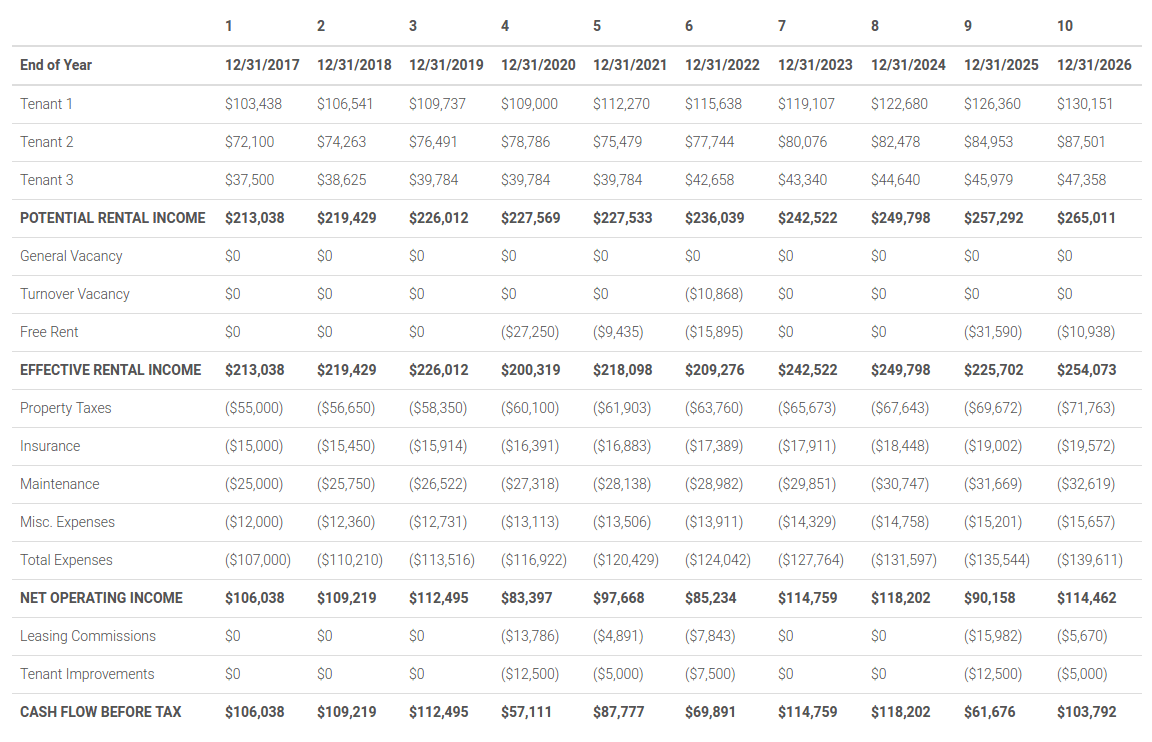

Now that we’ve walked through the calculations for Tenant 1, let’s see what our proforma looks like when we input market leasing assumptions for all 3 tenants. Using our Proforma Software, this entire analysis took just a few minutes to complete:

As you can see in the completed proforma above, the rental income for Tenant 1 in years 4-10 is exactly what we calculated step by step above. This same process was repeated for Tenant 2 and Tenant 3. You’ll also notice that the market/renewal leasing commissions and tenant improvements are calculated at the start of each market/renewal term. Additionally, free rent is automatically calculated on a separate line item. Finally, for Tenant 3 we assumed there would be 4 months of downtime if we had to find a new tenant for the space. You’ll notice that this is taken into account in the above proforma as well with the Turnover Vacancy line item.

Conclusion

Market leasing assumptions are often a key component in a commercial real estate analysis. However, since there are so many moving parts, market leasing assumptions are often confusing to many commercial real estate professionals. In this article we walked through how market leasing assumptions work, step by step. We also looked at an example office building case study where market leasing assumptions allowed us to make reasonable assumptions about what happens after tenant leases expire.